The Stack You're Actually Betting On

The Impact Architecture, Layer 3 — part 7 of the ROAD series.

Part 6: The Price Tag Isn’t the Price

On March 23, 2021, just over a month into the CEO job, Pat Gelsinger announced that Intel would do three things at once. Keep running its own fabs. Use external foundries like TSMC for some designs. Stand up a new business — Intel Foundry Services — selling Intel’s process capacity to external customers. The package came with a $20 billion commitment for two new fabs in Arizona. He called it IDM 2.0. [1]

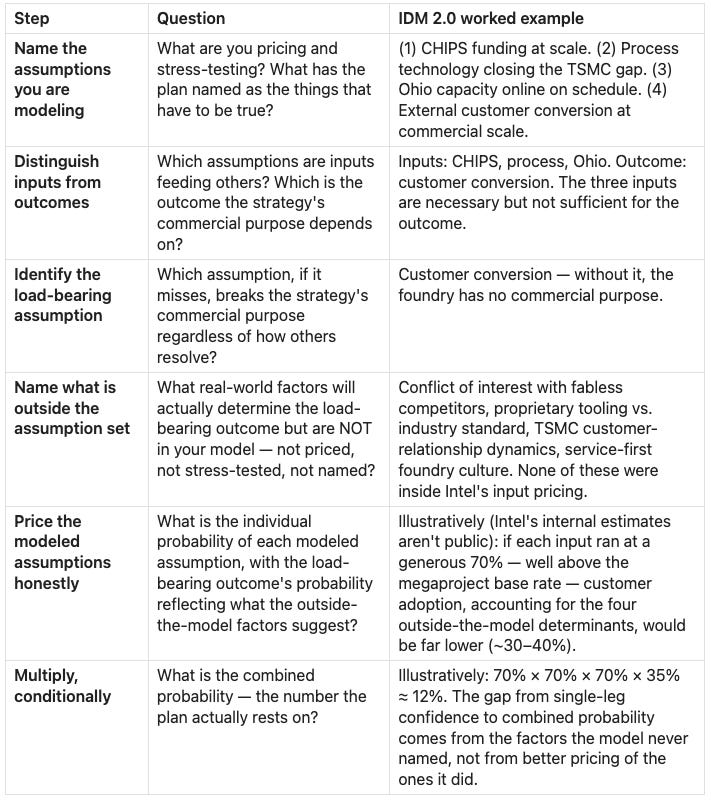

What Intel announced was not one bet. It was four — and the four weren’t independent. Three of them — CHIPS Act capital, process technology, and the Ohio mega-site — were capabilities Intel needed in any case for its own products, scaled up for the foundry-services expansion. They were inputs feeding the fourth bet: whether external customers would choose Intel’s foundry over TSMC at commercially meaningful scale. That fourth bet — customer conversion — was the outcome specific to the foundry expansion. The inputs had to land for the outcome to be possible. The outcome had to land for the foundry strategy to mean anything commercially. Of the three inputs, technology mattered most: no fabless customer migrates to a foundry whose process can’t compete.

Four years later, the scorecard was mixed across the inputs but settled where it had to: at the outcome. CHIPS Act funding arrived; the August 2025 conversion to an $8.9 billion U.S. government equity stake helped catalyze roughly $7 billion of follow-on private investment from Nvidia and SoftBank. Process technology delivered four of five planned nodes, with 18A entering high-volume production in late 2025 and shipping its first consumer product at CES 2026. The Ohio mega-site, scheduled to begin producing chips in 2025, was pushed to 2030 — a five-year slip. Two input bets held with delays. One missed. None of that, on its own, would determine whether the foundry succeeded. [2]

What would was whether external customers chose Intel’s foundry over TSMC at commercially meaningful scale. Intel announced partnerships with MediaTek (2022), Arm (2023), Microsoft (2024), and AWS. The announcements were real; the revenue was not. Intel Foundry’s external-customer revenue fell from about $953 million in 2023 to roughly $307 million in 2025. The marquee announcements did not turn into product-level wins at commercial scale, and Intel’s own flagship Arrow Lake chip was moved off Intel 20A to TSMC. The outcome bet missed despite the inputs largely delivering. [3][4]

The usual explanations for why customers didn’t convert are that the bet was too big, or too late, or that Intel’s manufacturing execution couldn’t catch TSMC. Each is true in a local sense. None captures the pattern underneath.

IDM 2.0’s public framing treated customer adoption as a function of execution on the three inputs — capital plus process plus capacity, and customers would follow. The factors that actually decide whether fabless customers move to a new foundry — trust in IP isolation, design-flow switching cost, the customer-relationship signal at TSMC, and operating-model fit — sat outside that framing.

The case the public saw treated all four bets at the confidence of single independent commitments. The reality was a stack with structural correlation — three inputs feeding one outcome — and an incomplete framing that left the actual determinants of the outcome outside the analysis. What the public framing priced wasn’t what was actually deciding the outcome. That gap is the pattern most strategic bets that “should have worked but didn’t” turn on.

Strategic bets that should have worked but didn’t tend to have two things in common. The bet is a stack — several assumptions, all of which have to hold — so the real probability is much lower than any single piece. And the factors that actually decide whether the bet pays off are usually not in the assumption set at all.

R.O.A.D 3.3: Stress-test the assumptions — including the way they multiply

With the structure named, the 3.3 walkthrough takes the four bets one at a time — three inputs first, then the load-bearing outcome — and shows what was actually being asked alongside each that the public framing didn’t price.

The three input bets

Input 1 — CHIPS Act funding had to arrive at roughly the scale Intel was planning to spend. The Biden administration’s March 2024 preliminary award came in at $8.5 billion; November’s final agreement was $7.86 billion. By August 2025 the grants had been converted into an $8.9 billion U.S. government equity stake, and that deal helped catalyze roughly $7 billion of additional private investment from Nvidia and SoftBank in the months that followed. The capital arrived. The expansion was funded — through CHIPS and through the follow-on private investment the government stake helped unlock. Of the four assumptions in the stack, this is the one that held. [3]

Input 2 — Intel’s process technology had to close the gap with TSMC. Chipmakers measure each manufacturing generation as a “process node” — for decades named by feature size (14nm, 10nm, 7nm), with smaller numbers meaning more advanced. By 2021 Intel was visibly behind TSMC on that scale and rebranded the next five generations as Intel 7, Intel 4, Intel 3, Intel 20A, and Intel 18A. The “five nodes in four years” roadmap promised to deliver all five between 2021 and 2025 — roughly the time most chipmakers ship two. Intel 7 shipped. Intel 4 reached high-volume manufacturing in September 2023, late. Intel 3 shipped in 2024. 20A was cancelled for product use in September 2024, with Arrow Lake moved to TSMC. 18A entered risk production in early 2025, moved to high-volume production in late 2025, and shipped its first consumer product — Panther Lake — at CES 2026. Four of the five planned generations delivered, with delays; the fifth was cancelled and its workload absorbed by the next. The process bet largely held. [5]

Input 3 — The Ohio mega-site had to come online on the announced schedule. Originally a $20 billion initial commitment, up to $100 billion over a decade, with the first fab producing chips by 2025. In February 2025 the first-fab production date moved to 2030; the second to 2031. The political story around CHIPS Act support had counted on those ribbon-cuttings happening inside the original investment window. The Ohio schedule slipped roughly five years. [6]

Across the three inputs, two held with delays and one missed materially. By the input scorecard alone, IDM 2.0 was running a recoverable execution problem.

The outcome bet — and the factors outside the model

The outcome bet — external customers had to choose Intel’s foundry over TSMC at commercially meaningful scale.This is where the strategy’s commercial purpose lived. The marquee partnerships — MediaTek (2022), Arm (2023), Microsoft (2024), AWS — were announced. The revenue was not. Intel Foundry’s external-customer revenue in 2023 was about $953 million. The TSMC comparison flatters Intel — TSMC is much larger, and a small absolute number against TSMC is not by itself disqualifying. The harder test is whether Intel was on the ramp its own plan required. External revenue fell from about $953 million in 2023 to roughly $307 million in 2024, and stayed near that level in 2025 — the line moved opposite to the trajectory the marquee partnerships implied. Intel’s own flagship Arrow Lake chip was moved off Intel 20A to TSMC. By every disclosed measure, the customer-acquisition bet had not begun to convert. [4]

The factors that actually drove the customer outcome are the part most discussions of Intel’s foundry strategy skip. They share a property: none of them appears in IDM 2.0’s public framing. The public framing priced whether the inputs would land. These four factors were determining whether customers would actually move, and they sat outside the framing entirely.

Four such factors have been visible in industry analyst commentary since 2021. The competitor-as-supplier problem: fabless customers don’t trust their proprietary designs to a foundry that also competes with them in their end markets. Design-flow lock-in: existing TSMC-anchored designs take roughly 12 to 18 months to port to Intel’s process per SemiAnalysis, and Intel’s PowerVia backside-power architecture forces redevelopment of IP blocks built for front-side power. The customer-relationship signal at TSMC: advanced-node capacity has been sold out years in advance, yet those customers chose to wait at TSMC rather than port to Intel — evidence that the other factors were doing the deciding. The operating-model mismatch: Intel built a product business that owns its own roadmap; TSMC built a service business that follows customers’. None of these appear in IDM 2.0’s public framing.

What is not visible in Intel’s public actions is any measure that materially moves these four. There has been no spin-off of the product business that would remove the competitor-as-supplier problem. No disclosed port-cost subsidy that would break the design-flow lock-in. No public restructuring of operating-model metrics or customer contracts that demonstrates the service-first pivot in practice. Lip-Bu Tan, in his April 2025 speech as CEO, named the cultural distance — “Foundry is a service business... built on the foundational principle of trust” — but naming a distance is not closing it. The four factors were load-bearing in 2021 and they remain load-bearing now. The feedback loop that should turn marquee announcements into product-level wins at commercial scale has not begun to move. Stress-testing the four assumptions Intel did name was never going to catch what was actually deciding the outcome. [7]

The math pricing the bet

The math is straightforward. Even if each of Intel’s four assumptions sat at a generous 70 percent probability — well above the one-in-ten on-time-on-budget rate Flyvbjerg finds across megaprojects — the combined probability of all four holding is 70 to the fourth, or 24 percent. Three of the four were inputs to the fourth, and the actual determinants of the fourth lived outside Intel’s model entirely, so the realistic number is closer to 10 percent. The point isn’t the precise probability. The point is that a strategy publicly framed at high single-leg confidence on every piece was running a combined bet much closer to 10 percent than to 70.

Making a low-probability bet is not by itself the failure. AWS, the iPhone supply chain, and Microsoft’s cloud pivot were each multi-assumption bets at uncertain combined probability, and each paid off. What distinguished them was sequencing — committing to each successive leg only after the prior one had shown a real signal, with the irreversible commitments arriving late, not concurrent. The failure mode is committing to every leg of a stack at once, as if each were an independent high-probability bet. Doing all the legs concurrently compounds the risks instead of compounding the success. The math isn’t a verdict on the bet. It’s a verdict on how the commitment is structured over time.

The mental model: when a plan requires several things to hold at once, the odds of the plan are the odds of each piece multiplied together, not averaged. When some of those pieces are inputs to others, the math runs through the conditional probabilities. And when the load-bearing outcome’s actual determinants are factors the model never named, the plan’s real probability is much lower than the simple multiplication suggests. The response to that math isn’t better pricing of the assumptions you already named — it’s restructuring the commitment so each leg validates before the next one commits.

Three things make this worse in practice. Consensus reads as confirmation — four people each saying “70 percent likely” about their own assumption is not a 70 percent plan; it’s four 70 percents that all have to cash at once, often conditioned on each other. Easy assumptions get stress-tested; hard factors get left out of the model — teams build sensitivity tables for cost and timeline but assert competitive response, customer trust, and cultural mismatch in prose, or leave them out entirely. Internal estimates beat external base rates — “we’re not like the other megaprojects; we have specific reasons” is the signature sentence of the assumption stack, and Flyvbjerg’s data still shows roughly one in ten large projects deliver on time and on budget.

What to do when the bet is a stack

Four moves act on the math.

Sequence the validation. Find the cheapest credible signal of the load-bearing outcome and require it before committing irreversible capital.

Define kill criteria. Name in advance what would tell you the load-bearing assumption isn’t holding — a missed milestone, a customer threshold, a competitor or regulatory move. Their job isn’t cancellation; it’s forcing an honest re-pricing while the next tranche of capital is still recoverable.

Structure for optionality. Separate the part of an input investment justified by the stack from the part that stands on its own, and approve them under separate kill criteria.

Defer the irreversible. Some commitments reverse cheaply (announcements, marketing posture, organizational structure); some don’t (capital projects, locked-in supplier contracts, regulatory commitments). Stage the irreversible behind milestones on the load-bearing assumption.

These four reduce the cost of being wrong, not the uncertainty itself. (Layer 2 covers how to identify the load-bearing assumption; without that, the 3.3 stress-test runs on the wrong variable.)

The stack stress-test

Strategy Smell: “We have three independent reasons to believe this will work.” That phrasing should trigger two checks. The multiplication check — independent reasons are multiplicative, not additive. And the completeness check — what determines whether the outcome actually happens, and is any of it outside the three reasons you’ve named?

R.O.A.D 3.4: Build the decision package — give decision-makers the picture they need

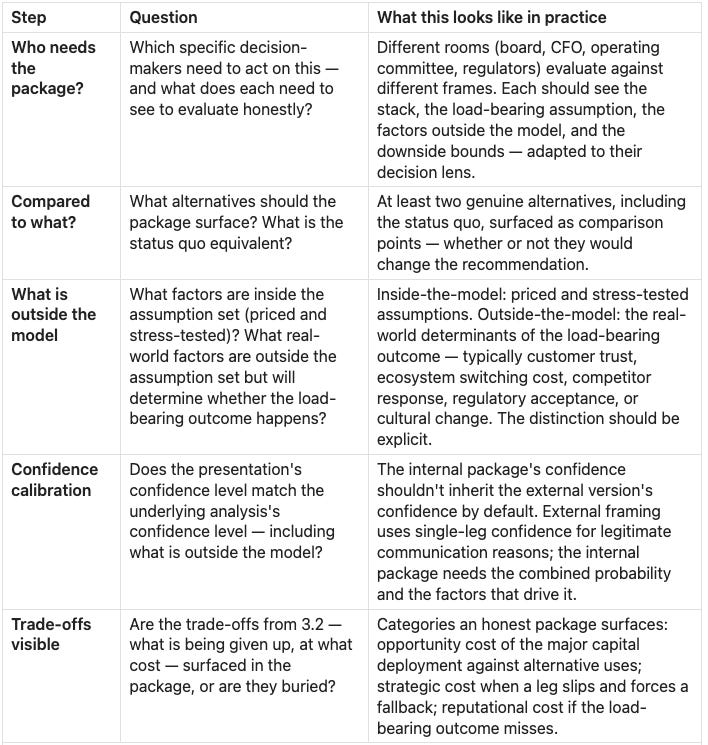

A decision package has one job: give the people approving the bet an honest picture of what they are about to approve. Not the picture that wins approval. The picture that lets them make a real decision.

That job has four components.

First, it names what is being decided — the specific bet, in the terms the decision-makers think in (capital structure, expected returns, time horizon, organizational commitment).

Second, it surfaces the alternatives — at least two genuine ones, including the status quo, so the decision is relative rather than absolute.

Third, it carries the math and the model’s boundaries — the assumption stack from 3.3, the distinction between input bets and outcome bets, the load-bearing assumption, the factors outside the assumption set that will determine the load-bearing outcome, and the trade-offs from 3.2. Decision-makers see what they are betting on, what they are giving up, and what lives outside the model they’re about to approve.

Fourth, it calibrates the confidence — the presentation’s confidence level matches the underlying analysis’s confidence level, so the certainty in the prose corresponds to the certainty in the math.

When a package does these four things, the bet may still fail — but it fails as a priced bet rather than as a surprise. When the package fails to do these four things, the bet is approved at a confidence level the analysis cannot defend, and the organization is unprepared for the more likely outcome.

The mental model: the decision package is where analysis becomes visible to the people approving the bet. Decision packages are advocacy by design — you wouldn’t bring one to the board if you didn’t believe in it, and persuading the room is part of the job. What separates honest advocacy from dressing-up is whether the rigor was done upstream and whether the analysis’s limits — the stack math, the load-bearing assumption, the unmodeled determinants — are surfaced inside the package rather than smoothed out of it. The operator’s responsibility is the honesty of the underlying analysis and the visibility of its limits, not the suppression of persuasion.

What we can see externally is the pattern of communication: uniformly confident single-leg framing across all four bets, from “Intel Unleashed” (March 2021) and the “five nodes in four years” commitment to CHIPS advocacy and customer-acquisition pitches. None surfaced the stack math or the factors outside the assumption set.

Intel’s internal package isn’t public, so the lesson isn’t whether their analysis was right. It’s the pattern. When external framing on a multi-assumption strategy is uniformly confident across each leg, there are two operator implications. From outside — as a competitor, investor, or counterpart — read that uniform confidence as a signal that the internal stack math may not have been forced into the room. From inside, your job is to make the internal version carry what the external version, for legitimate communication reasons, does not: the stack, the load-bearing assumption, the factors outside the model. External advocacy and internal honesty are different jobs.

Four recurring failure modes show up in decision packages — general patterns, not Intel-specific. Recognize them in real time, whether you’re building the package or reviewing it.

The package is shaped around the audience easiest to convince. Language built for supportive audiences doesn’t survive board or CFO stress-testing — and doesn’t give skeptical decision-makers the picture they need.

The “compared to what?” question gets skipped. Business cases evaluate a strategy in absolute terms; decision-makers evaluate in relative terms. Rough analysis of three alternatives almost always beats deep analysis of one.

Confidence signals get treated as commitments. Roadmap dates and capex ranges get framed with external credibility in mind, then become the internal plan of record. Slips read as failures rather than forecast errors, and high-confidence framing reduces the organization’s readiness to adapt when reality diverges.

Dressed-up advocacy. The tell: the “analysis” considered one option in depth, and the factors outside the assumption set were either not named or folded into the modeled assumptions as if better execution would handle them. When that happens, the rigor wasn’t done; the case was assembled.

The decision-package check

Strategy Smell: “The case is ready to present.” Decision packages don’t get cleaner by getting shorter — they get cleaner by surfacing the stack. When someone says the case is ready, ask what got simplified out.

Adapting both blocks to your context

Any multi-assumption initiative needs both checks — the multiplication math and the structural response. Math is a verdict on how the commitment is structured over time; sequencing is the response. The outside-the-model check applies whenever the load-bearing outcome depends on customer trust, ecosystem switching cost, regulatory acceptance, or cultural change. The math is identical at $100 million and $100 billion — but smaller bets have less margin to absorb a miss whose cause was never on the page.

A useful final check: if the harshest skeptic on the team were running the case, what would they name that the current case has left out? If the answer is “everything that matters,” the case is assembled, not analyzed.

The Layer 3 close

Layer 2 gets you to the structural source and the highest-leverage intervention. Layer 3 asks whether the bet on that intervention is one the organization can afford to lose — and whether the analysis presented to decision-makers gives them a fair chance to see what they are approving.

Stress-testing the stack isn’t refusing to bet. It’s knowing what bet you’re making, and sequencing the commitment so the irreversible pieces follow the load-bearing validation. Building an honest decision package isn’t rejecting advocacy. It’s giving decision-makers the picture they need, not the picture they will most easily approve.

Next week: Layer 4 — Deliver the Impact

Stress-testing and packaging get you to a decision. The decision gets you nowhere until the organization can actually execute against it. Layer 4 is where the strategy either becomes real impact or dies in the handoff. Four blocks: mapping the stakeholders who were not on the original list, designing the narratives that different audiences need to hear, architecting the decisions that translate strategy into thousands of operational choices, and building the feedback loops that tell you whether execution is working — or whether the ground has shifted under the plan.

If this resonates

Subscribe. The ROAD series publishes weekly.

Background information

The CHIPS Act — short for the CHIPS and Science Act, signed by President Biden in August 2022 — appropriated about $52 billion in semiconductor-related federal funding, of which $39 billion was direct manufacturing subsidies, designed to pull semiconductor manufacturing back onshore after decades of concentration in Taiwan and South Korea. Intel had been positioning for those subsidies since early 2021. The other anchor is TSMC — Taiwan Semiconductor Manufacturing Company — the contract chipmaker that Apple, Nvidia, and AMD pay to physically manufacture their chips, and the company Intel had fallen behind. IDM 2.0 was simultaneously a competitive bet against TSMC and a political bet that CHIPS Act dollars would arrive on time.

Sources

[1] Intel IDM 2.0 announcement, March 23, 2021: https://www.intc.com/news-events/press-releases/detail/1451/intel-ceo-pat-gelsinger-announces-idm-2-0-strategy.

[2] Intel and Trump administration equity agreement, August 22, 2025: https://www.intc.com/news-events/press-releases/detail/1748/intel-and-trump-administration-reach-historic-agreement-to. Nvidia $5B Intel investment, announced September 18, 2025; SoftBank $2B Intel investment, August 2025.

[3] CHIPS Act preliminary award, Department of Commerce, March 20, 2024. Intel CHIPS Act finalization at $7.86B, November 26, 2024. Intel equity conversion, August 22, 2025 (Intel press release cited in [2]).

[4] Intel 2023 Foundry segment restated financials, April 2, 2024 (8-K). Intel 2024 10-K segment reporting: external foundry revenue $307M. Q4 2025 disclosures: 2025 external foundry revenue $307M.

[5] Intel Accelerated roadmap, July 26, 2021. Intel 4 high-volume manufacturing announcement, September 29, 2023. 20A cancellation for product use, Q3 2024 earnings commentary. Panther Lake (Core Ultra Series 3) launch announcement, CES 2026.

[6] Intel Ohio announcement, January 21, 2022: https://www.intc.com/news-events/press-releases/detail/1521/intel-announces-next-us-site-with-landmark-investment-in. Ohio delay announcement, February 28, 2025 (per CNBC and Manufacturing Dive).

Base-rate references: Bent Flyvbjerg et al., How Big Things Get Done (2023); Flyvbjerg & Budzier, “Why Your IT Project May Be Riskier Than You Think,” Harvard Business Review, 2011; Flyvbjerg, “How common and how large are cost overruns in transport infrastructure projects?” Transport Reviews 23(1), 2003.

Structural-barrier context (foundry industry dynamics): industry analyst commentary across the Intel Foundry Services period 2021–2025, including SemiAnalysis, Bernstein semiconductor research, and Intel’s own foundry-customer disclosures around tooling and process-design-kit ecosystem development.

[7] Structural barriers in foundry-customer adoption:

Conflict of interest / partner-competitor framing: Reed Hundt (former Intel board member) public commentary on the case for spinning off Intel Foundry — see WCCFTech, “Intel’s biggest problem is being a partner-competitor at the same time”; Fudzilla, “Intel’s foundry problem is trust”; SiliconANGLE, “Intel Foundry: bold bet filled with uncertainty” (Feb 10, 2024).

TSMC pure-play moat framing: Morris Chang public statements (”We sell service... we don’t sell products. Our customers sell products.”), covered by Quartr and Benzinga; IESE Insight on TSMC’s geopolitics-operations strategy.

EDA / PDK / port-cost claims: SemiAnalysis, “Is Intel Back? Foundry and Product” (April 2, 2024) — 12-to-18-month port estimates, PowerVia incompatibility with front-side-power IP. Synopsys press release (Feb 21, 2024) and Siemens (2025) on Intel 18A EDA certification.

TSMC capacity-queue data: Dataconomy, “TSMC’s advanced chip capacity is booked out through 2028” (Mar 2026); Silicon Analysts Q1 2026 lead-time and allocation reporting.

Intel 18A vs TSMC N2 technical comparison: TechInsights commentary via Tom’s Hardware (”Intel’s 18A and TSMC’s N2 process nodes compared”), and EE Times analyst coverage on TSMC’s 2nm leadership.

Lip-Bu Tan public statements on the foundry-service trust model: Tom’s Hardware coverage of Tan’s first speech as CEO (April 2025); The Register, “New Intel CEO major speech” (April 1, 2025).

Customer-conversion outcome and Intel’s own assessment: Intel SEC filings (full-year 2025 disclosures); CFO Q3 2025 commentary on commitments “not significant”; Lip-Bu Tan Q2 2025 earnings comments on “invested too much, too fast, without sufficient demand”; CNBC and Tom’s Hardware coverage.